Weekend Talking Points - 'Oil, Inflation & Rates'

With the US/Iran peace process underway, oil prices have fallen back to pre-war levels, but mortgage rates remain high (due to concerns about the Fed’s hawkish tilt). But inflation may have already peaked, and mortgage rates should follow inflation lower.

Oil prices are at pre-war levels. Before the start of the US/Iran war (2/27), West Texas Intermediate oil prices (“WTI”) were at $67/barrel. Once the war started, oil prices quickly moved above $100/bbl and peaked at $117/bbl in early April. But since the 6/17 signing of the MOU to end the war, oil prices have quickly retreated to near pre-war levels ($70/bbl).

But mortgage rates have remained frustratingly high. As the table above shows, US Treasury yields and mortgage rates have only just started to follow oil prices lower. That’s mainly because the bond market was spooked by the Fed’s recent hawkish (inclined to raise rates) tilt. But as inflation slows — and it certainly will if the peace remains intact — rates should eventually follow oil prices lower.

TP: In addition, I think the market has misinterpreted new Fed Chair Kevin Warsh’s focus on achieving ‘price stability’. We know that he believes rates should be lower (lagging and skewed inflation data, guesstimates etc.), that AI will prove deflationary, and that the supposed trade-off between the unemployment rate and inflation (the Phillips curve) doesn’t exist.

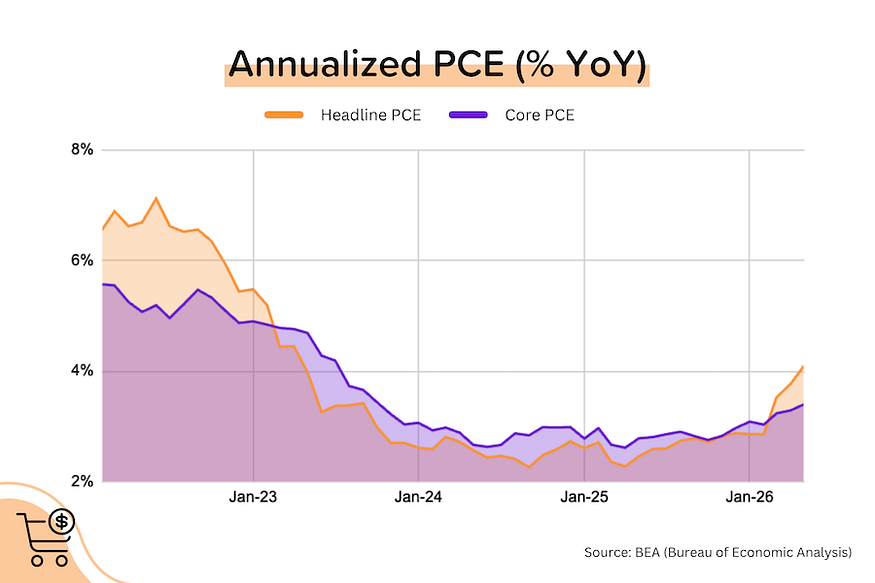

May PCE (inflation) jumped higher. The “headline” PCE index (Personal Consumption Expenditures = inflation for me and you) rose 0.4% month-over-month, lifting year-over-year “headline” PCE from 3.8% → 4.1%. That’s the highest annual growth since April 2023. “Core” PCE (which has been the Fed’s preferred inflation gauge) climbed 0.3% MoM, lifting YoY “core” PCE from 3.3% → 3.4%.

TP: The Fed’s inflation target is 2% for “core” PCE. But it has been above that target for over five years! At first (2021), much higher inflation was tolerated because the Fed expected it to be “transitory.” When it proved much more systemic, the Fed began raising interest rates aggressively in March 2022. “Core” PCE declined sharply over the course of 2024. In fact, we were getting very close to the Fed’s 2% target until Trump’s April 2025 “Liberation Day” tariffs set inflation on an upward trajectory, which got further boosted by the February 2026 US/Iran war.

New home sales falter. New home sales fell 13% month-over-month in May to an annualized pace of 580K new homes sold. That’s the 2nd-slowest pace of sales we’ve seen in nearly four years. The key issue is affordability: median new home prices are around $425K, and mortgage rates are in the mid-6% range. In addition, some large property investors may already be reducing purchases in anticipation of the upcoming ban on single family home purchases. [Census Bureau]

Bond and Mortgage Market

With oil prices already at pre-war levels, it’s only a matter of time before “headline” inflation comes down sharply. “Core” inflation will also move lower. While energy & food prices aren’t directly included in the “core” figures, higher energy prices sneak into the price of just about everything. And as the market (and the Fed members) begin to see inflation easing, expectations for rate hikes should fade.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- July 29 FOMC Meeting: 68% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 70% last week), and a 32% probability that rates will be 25 basis points HIGHER than they are today (was 30% last week).

- September 16 FOMC Meeting. 38% probability that the Fed Funds Rate will be kept at 3.50–3.75% (same as last week). But a 62% probability that rates will be at least 25 basis points HIGHER than they are today.

They Said It

“I hereby fully authorize the toll-free opening of the Strait of Hormuz and, simultaneously herewith, authorize the immediate removal of the United States Naval blockade. O ships of the world, start your engines. Let the oil flow!” — President Donald Trump on Truth Social