.jpg)

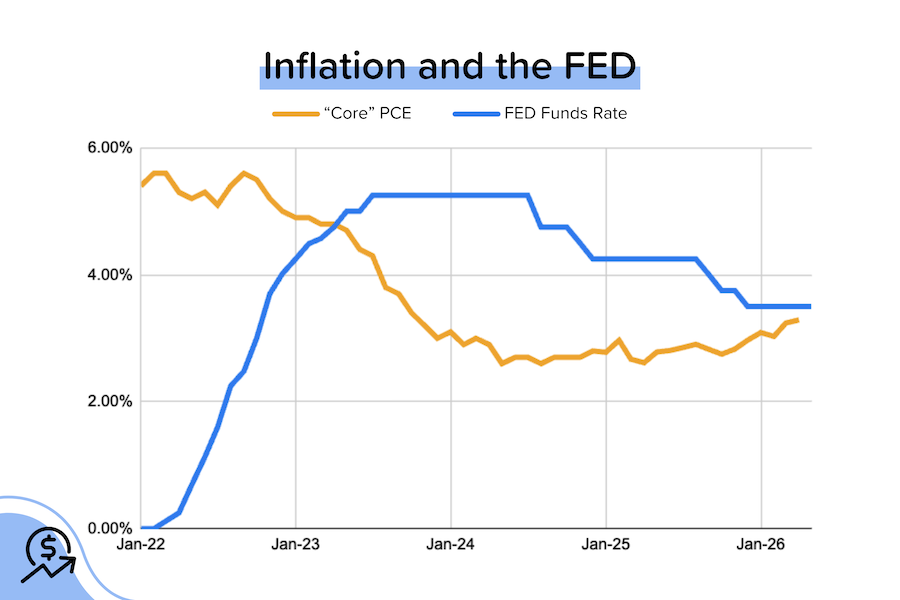

The Fed voted to keep interest rates steady, but many Fed members have a hawkish bias (wanting to raise rates). Over the last three months, energy prices have been driving inflation higher. But with the US/Iran conflict reportedly nearing an end, this should begin to reverse.

The war is over. Maybe. It looks real this time, but this has been a conflict where ceasefires meant ‘shooting at each other less’, so we can’t be certain. In any case, both the US and Iran have said that a deal has been agreed upon to open the Strait of Hormuz (Iran), unblock Iranian ports (US) and stop shooting (US, Iran, Israel).

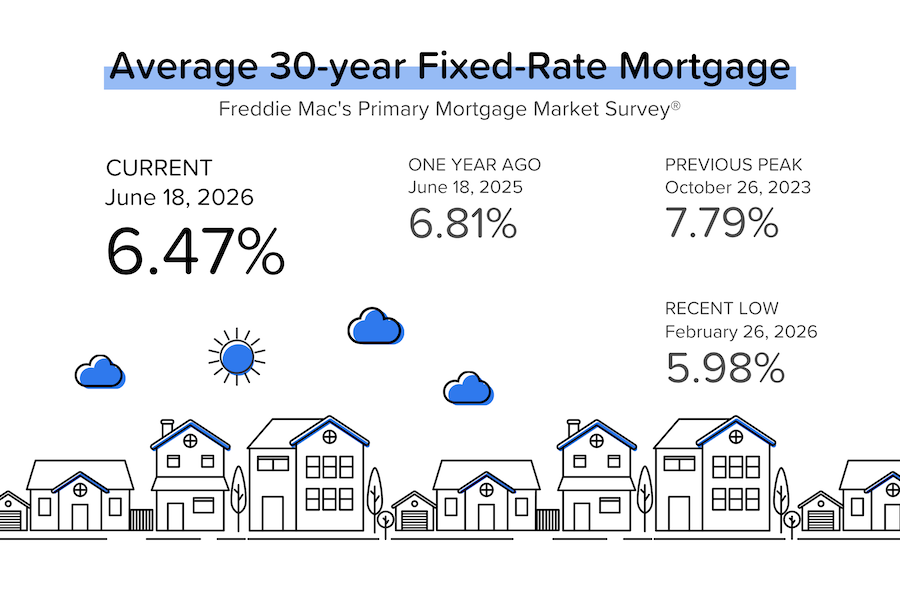

Oil prices are acting like the peace deal is real. Just before the start of the US/Iran conflict, WTI crude oil prices were at $67/barrel and average 30-yr mortgage rates were in the high-5% range. Today, WTI crude is at $75.50/barrel (just 13% above pre-war) and mortgage rates are at 6.50% (still 51 basis points above pre-war). Q: Can we get back to where we were pre-war? A: Only if inflation gets back on the path to 2%.

The Federal Reserve kept interest rates on hold. This was Kevin Warsh’s first FOMC meeting as Fed Chair, and he sounded surprisingly hawkish, which shocked the bond and stock markets. Fed members voted unanimously to keep rates steady. Chairman Warsh also kick-started his reform plans with the creation of a number of task forces to investigate things like the Fed’s communication policy. [Much more on this later.]

TP: Just imagine the tension! Mr. Warsh was appointed by President Trump, and has been critical of the FOMC for its backward-looking, “data-dependent” approach. And of course, ex-Chair (and frequent Trump whipping boy) Jerome Powell was in the room. In my opinion, Chairman Warsh wasn’t really being hawkish at all. He was just attempting to establish his inflation-fighting bona fides.

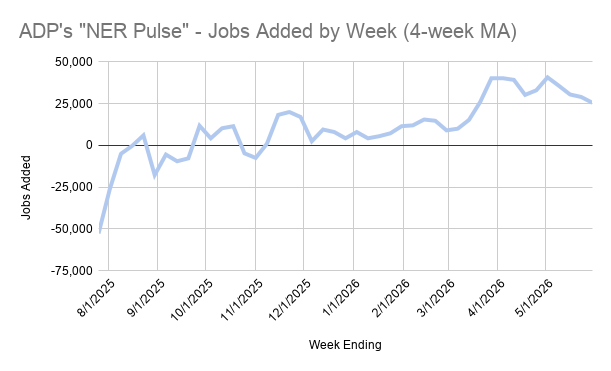

Weekly jobs growth slowed. ADP’s weekly “NER Pulse” reported that private job growth slowed further to an average of +25,500/week (or roughly 102K/month), down from +29,000/week the week earlier and +40,750/week a month ago. The downtrend implies that ADP’s June employment report will come in below the May’s +122,000 job figure.

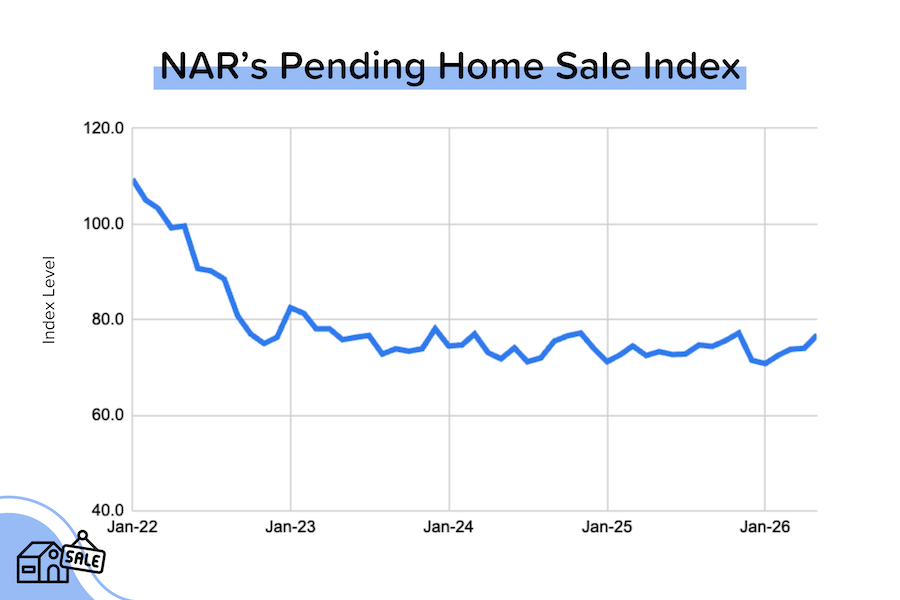

Pending home sales jumped in May. Despite higher mortgage rates, NAR's Pending Home Sales Index increased by 3.8% MoM in May to 76.8. That’s the fourth straight month of MoM improvement, and also the highest index level since November 2025. [NAR]

TP: So what’s going on here? According to NAR’s Chief Economist, Lawrence Yun, “A late spring buyer rush—even with mortgage rates not budging—is an indication of pent-up housing demand and consumers’ acceptance of above-6% mortgage rates as the new normal.”

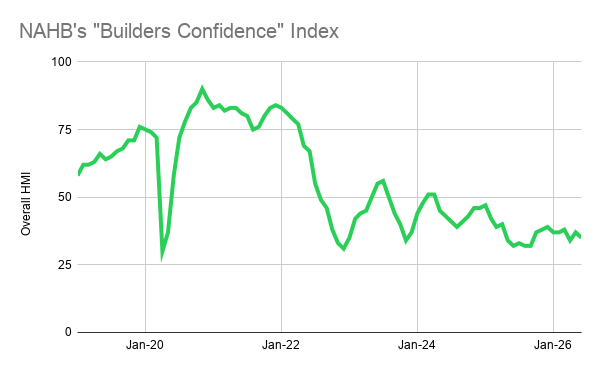

Builder confidence still in the dumps. The National Association of Homebuilders’ confidence index dropped 2 points to 35 (<50 = bearish, >50 = bullish) in June. The index has been below 50 since April 2024. The main issue: affordability.

Housing starts plunged. The pace of permit issuance for new homes was fairly normal at 1.4 million units (seasonally-adjusted, annualized rate), but housing starts fell 15% MoM (-9% YoY) to 1.2 million units (SAAR), the lowest figure we’ve seen in a very long time. Within that, multifamily starts were down an incredible 42% MoM (-9% YoY).

TP: I have a feeling like this will normalize next month. This is a highly volatile data series. That said, it’s a reminder that homebuilders are facing high vacancy rates, particularly in the South region.

We Need to Talk About Kevin

Kevin Warsh became the 17th Chair of the Federal Reserve on May 22, 2026. He returns to the Fed with a well-documented set of views that diverge meaningfully from those of his predecessor, Jerome Powell. Here’s what you need to know:

- He’s already a Fed insider. He joined the Fed’s Board of Governors in January 2006 as a member of Fed Chair Bernanke’s team. So he was there during the financial crisis, and saw firsthand the emergency policymaking (company bailouts, asset purchases etc.). He left the Board of Governors in 2011.

- He doesn’t like the 2% target. It started as an internal guideline under Greenspan, and became a rigid goal under Bernanke. Kevin thinks that this fixed target limits the Fed’s flexibility to react to unique circumstances. In his testimony to Congress, he defined price stability as “when no one’s talking about it [inflation].” This has echoes of Greenspan’s idea of price stability: a state in which expected changes in the general price level don’t materially affect business or household decisions.

- He understands the weaknesses of the current data sources. He has publicly discussed many of the issues that we’ve highlighted here (falling survey response rates, massive lags in the “shelter” data in CPI, birth/death model creating phantom jobs in the BLS report, etc.) He wants the Fed to have greater access to real-time market data, rather than always looking in the rearview mirror. He favors trimmed-mean averages for the inflation data [removing outliers from the basket of goods and services] because, “What I’m most interested in is the underlying inflation rate, not what’s the one-time change in prices because of a change in geopolitics or a change in beef prices.”

- He wants to kill the “dot plots.” Every quarter, Fed members make their predictions for key economic variables (inflation, the unemployment rate, GDP growth, the Fed Funds Rate, etc.) That’s the basis for the Summary of Economic Projections (SEP) report. Kevin believes that these projections bias Fed members’ reaction to new data. He wants the SEP to go. “Unlike many of my colleagues past and present, I don’t believe in forward guidance.”

- He doesn’t believe in the Phillips Curve. This influential theory (originally proposed in 1958!) posits an inverse relationship between unemployment and inflation. When rates are low and unemployment falls, wage pressures & inflation rise. So if a central bank wants to kill inflation, it must raise rates and accept that unemployment will rise. That’s the supposed trade-off, and central bankers around the world accept it as gospel. The problem is that the Philipps Curve is extremely simplistic and far from an economic ‘law’ - in fact, it rarely holds. That’s why Chairman Warsh said that “We don’t have to choose between inflation and jobs.”

- He wants a smaller Fed balance sheet. The Fed’s balance sheet peaked at around $9 trillion in early 2022 and is currently ~$7 trillion. It was just $900 billion before the financial crisis! Kevin sees Fed asset purchases as “fiscal policy in disguise” or “mission creep” (the Fed is only supposed to be in charge of interest rate policy). The issue is that cutting interest rates (his stated preference) and asset sales (which tend to raise market rates) often work in opposite directions.

In summary, the new Fed Chair wants the FOMC to be flexible and forward-looking, using the latest data, and less focused on making forecasts and public speeches. He wants FOMC meetings to be “messier” and believes that a “good family fight” (vigorous debate) will ultimately result in better Fed decisions. We shall see.

Bond and Mortgage Market

It seems that the bond market was hoping that Fed Chairman Warsh would show up and tell everyone that they were silly to be worried about inflation. Instead, he kept talking about the importance of maintaining ‘price stability’ (but that means something different to him, as I explained above), so the bond market sold off.

Rather bizarrely, the market is now pricing in a much higher chance of rate hikes than BEFORE Warsh took over. This strikes me as a bond-buying opportunity. We know that inflation will subside if the US/Iran war is truly over, and we know that Chairman Warsh has a bias towards lower rates.

Note: The Fed Funds Rate policy range is currently 3.50-3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- July 29 FOMC Meeting: 70% probability that the Fed Funds Rate will be kept at 3.50-3.75% (was 88% last week). But now a 30% probability that rates will be 25 basis points HIGHER than they are today (was 11% last week)!

- September 16 FOMC Meeting. 38% probability that the Fed Funds Rate will be kept at 3.50-3.75% (was 62% last week). Now a 48% probability that rates will be 25 basis points HIGHER than they are today (was 34% last week) and a 14% probability that rates will be 50 basis points higher.

They Said It

"We've missed (on inflation) for five years and we're going to fix that. When we deliver on our price stability objectives, which we will, the American people will feel as though the hardships that they've been living through...are in the rear view mirror." - Kevin Warsh, new Chairman of the Federal Reserve

“Costly and inefficient regulatory policy is clearly impeding the ability of builders to increase the housing supply. According to a new NAHB study, government regulation, taxes, fees and other costs add more than 26% to the price of an average single-family home. Easing permitting bottlenecks, density limits and inefficient zoning rules would help reduce costs and support the housing growth the nation needs.” - Robert Dietz, NAHB’s Chief Economist

Related posts

FAQ: Will paying off my credit cards before applying for a mortgage help?

.png)

Annual Inflation Eases, Fed Leaves Rates Unchanged

FAQ: Can I make a big purchase before closing on my home?

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.