Mortgage rates are trending lower, a Fed rate cut is highly likely in September, home prices are falling (modestly) in many markets, and buyers are regaining negotiating power. It’s still tough out there for buyers, but affordability is certainly improving at the margin.

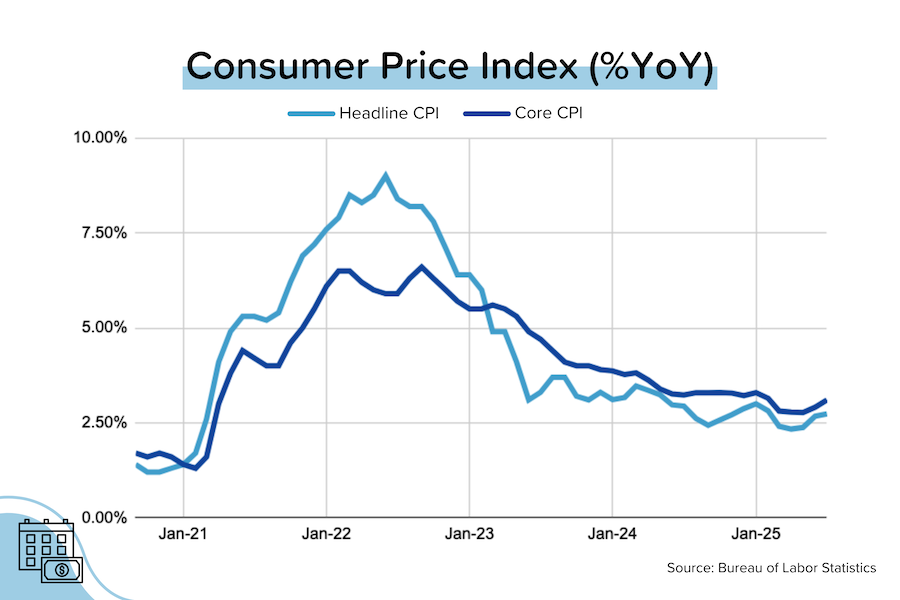

CPI: When just OK is good enough. July “headline” CPI was flat at +2.7% YoY, but “core” CPI rose to +3.1% YoY (from +2.9% YoY in June). There were signs of tariff impacts on some items (fresh fruit, coffee, furniture etc.) but these products have tiny weightings in the overall index. Shelter cost growth (~44% weighting in the “core” index) slowed to +3.7% YoY (from +3.8% YoY), and Energy costs (~7% weighting in the “headline” index) fell 1.1% month-over-month. [BLS]

TP: Was this a massively encouraging inflation report? No. Annual “core” CPI has now risen for two straight months, which means that we’re getting further away from the Fed’s 2% target. That said, I think the report was “good enough” in that it: 1) wasn’t as bad as feared, and 2) shouldn’t dissuade the Fed from cutting rates at their next meeting on September 17.

MBS Highway Housing Survey results for August. After plunging 8 points in July (to 26), our National Housing Index lost an additional 2 points in August (to 24). That is the lowest index level we’ve seen since January 2023, when home prices were briefly drifting downward in the wake of the Fed’s aggressive tightening cycle. [MBS Highway]

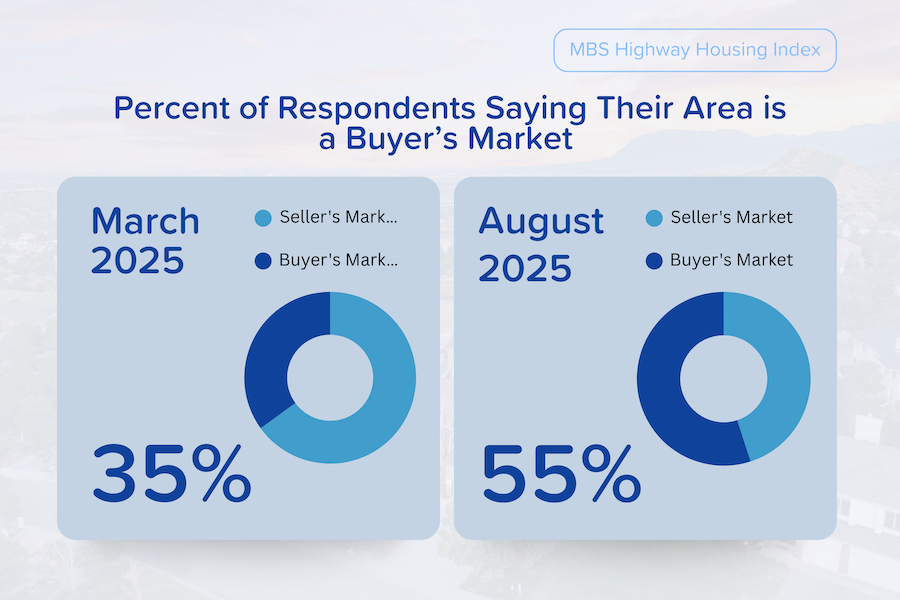

More buyer’s markets. The Question of the Month for the MBS Highway Housing Survey was “Are you operating in a buyer’s or seller’s market?” We asked the same question in March 2025. Six months ago, only 32% of respondents said that buyers had the upper hand in negotiations. This month, 55% of respondents said that they were operating in a buyer’s market.

TP: You probably guessed that Florida (83% of respondents) and Texas (72%) were two of the states where the majority of respondents said “buyer’s market”. But there were 7 other states where more than 70% of respondents said “buyer’s market”: Mississippi (100%), Arizona (91%), Tennessee (87%), Arkansas (80%), Colorado (80%), Oklahoma (75%), and Utah (75%).

Bessent wants 50 bps. Treasury Secretary Scott Bessent publicly opined that the Fed Funds Rate (“FFR”) was 150–175 bps too high, and that the Fed should cut rates by half a percentage point at its September meeting. The bond market loved that. [Reuters]

TP: Of course, Bessent doesn’t get to vote, and the Fed is meant to be independent. But with Trump confidant Stephen Miran named as the new Fed Governor (replacing the outgoing Adriana Kugler), and the Fed Chairmanship still up for grabs, dovish voices will doubtless grow in volume.

By the way, if the FFR moved 175 bps lower from where it is today, it would be 2.75%. Assuming the same spread between the FFR and average 30-yr mortgage rates (currently 200 bps), that would mean 4.75% for mortgage rates! We’d be off to the races again!

“Underwater” mortgages rise, but this ain’t 2009. According to ICE data, 1% of US home mortgages were underwater at the end of April 2025. In comparison, 23% were in negative equity at the end of September 2009. Submerged mortgages are much more prevalent in certain Florida and Texas cities (Cape Coral FL — 7.8% of mortgages, Lakeland FL — 4.4%, San Antonio TX — 4.3%, Austin TX — 4.2%), but the nationwide impact is (so far) quite limited. [ICE, ResiClub]

Definition: An “underwater” mortgage is when your home is worth less than what you still owe the bank. This usually only happens if prices drop more than your down payment. For example, with 20% down, prices would have to fall over 20% for you to be underwater, which is also called having “negative equity.”

TP: There are a number of reasons why most mortgages still have their head above water. First, because home prices have only recently started to fall, and then not much. You pretty much had to buy at the worst possible time and with a low down payment to be underwater. Second, if you’ve owned the property for a few years, you’ve added to your equity through normal mortgage payments. In other words, the buffer is larger than your initial down payment percentage.

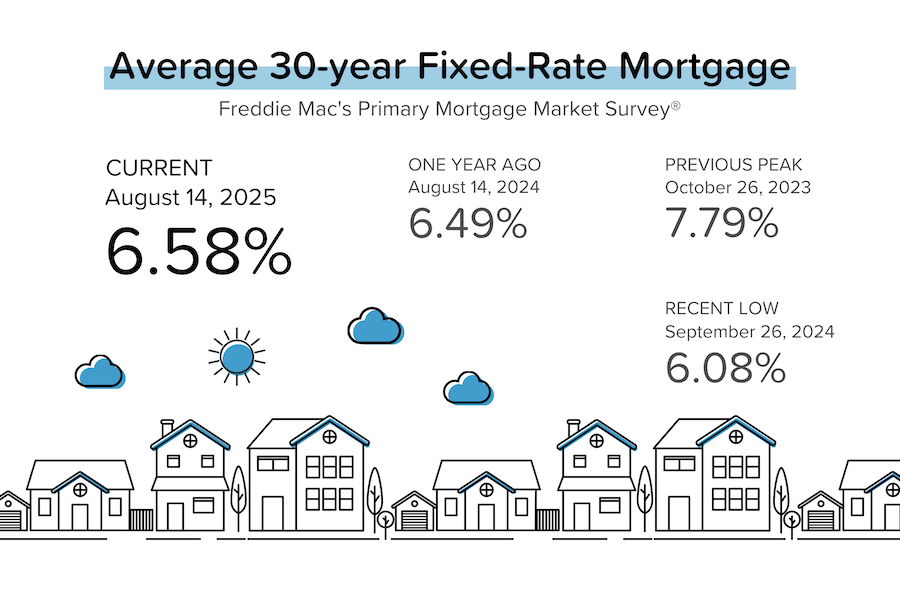

Mortgage rates approach 6.5%. We’re agonizingly close to a rebound in transaction volumes. According to Freddie Mac’s weekly PMMS survey of lenders, the average 30-year mortgage rate was 6.58%. We’ve already seen a sharp increase in refi volumes (the refi reaction to lower rates is pretty much immediate), but it takes time for purchase transactions to get going again. For people to start buying homes, it’s just about rates going lower, it’s about them staying lower. [Freddie Mac]

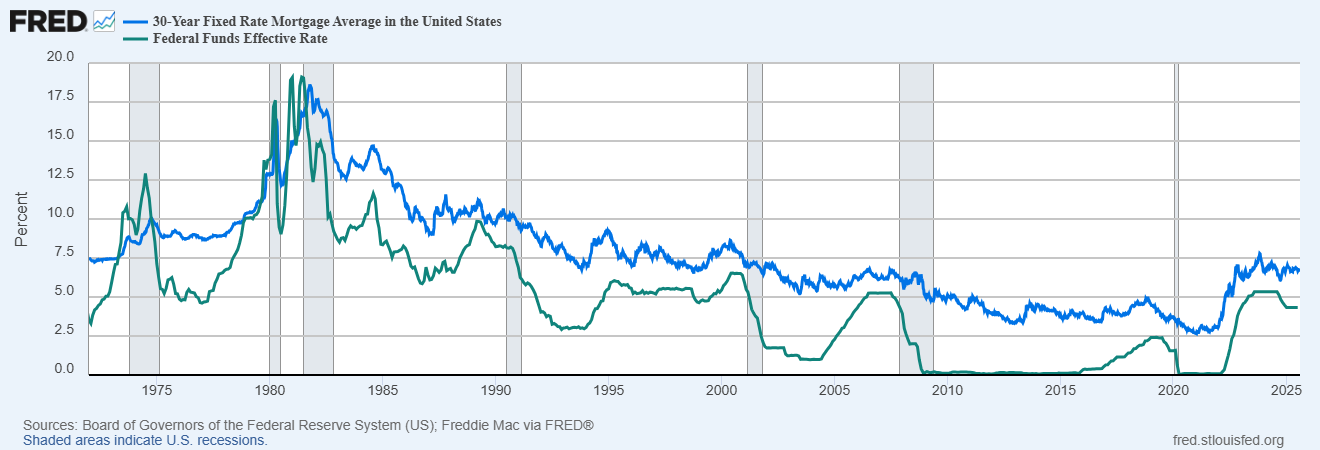

Mortgage rates tend to follow the Fed Funds Rate. Skip this if you already know how all this works. First, the Fed does NOT set mortgage rates. Instead, the Fed determines the target range for the Federal Funds Rate (the overnight borrowing rate between banks), and every other fixed income instrument (bank deposit rates, CDs, US treasury bonds, mortgage backed securities, mortgage rates) is influenced by the FFR.

While the FFR and mortgage rates can move in different directions in the short term (and the relationship is not 1:1), over the long term, the correlation is clear (see graph below). It’s also pretty clear that when the Fed is cutting the FFR aggressively, we’re usually already in a recession.

Blue line: Average 30-yr Mortgage Rate; Green line: Effective FFR

TP: One source of confusion for people is that market rates (like US bond yields, or MBS yields) will always anticipate Fed moves. The decline we’ve seen in mortgage rates over the last few weeks is (at least partially) already pricing in Fed rate cuts that haven’t happened yet.

Bond and Mortgage Market

Two weeks ago, the shocking BLS report (just 73K jobs added in July, and huge negative revisions to the May and June reports) sent mortgage rates lower. Expectations for 1–2 Fed rate cuts in 2025 moved up to 2–3. Then came the CPI report: it was just ok, but it seemed to convince the market that there was nothing in the way of a September 17 rate cut. The latest move was driven by Treasury Secretary Bessent’s call for a 50 bps cut on September 17, and 100–125 bps in further cuts after that.

Here’s what the Fed Funds Rate futures market is currently pricing in for rate cuts:

Note: The current Fed Funds Rate policy range is 4.25–4.50%.

- September 17 FOMC Meeting: A 94% probability that rates will be 25 bps below current (unchanged from a week ago). 6% probability that rates will be 50 bps below current (that’s new).

- October 29 FOMC Meeting: 63% probability that rates will be 50 bps below current (unchanged from a week ago). 4% probability that rates will be 75 bps below current (that’s new).

- December 10 FOMC Meeting: 53% probability that rates will be 75 bps below current (unchanged from last week). 3% probability that they will be 100 bps below current.

They Said It

“I think we could go into a series of rate cuts here, starting with a 50 basis-point rate cut in September. If you look at any model, it suggests that [the Fed Funds Rate] should probably be 150, 175 basis points lower [than it is today].” — Scott Bessent, US Treasury Secretary

“Fifty [basis points] sounds, to me, like we see an urgent [need to cut] — I’m worried it would send off an urgency signal that I don’t feel given the strength of the labor market. I just don’t see that. I don’t see the need to catch up.” — Mary Daly, San Francisco Fed President

Related posts

.jpg)

Weekend Talking Points - 'Backwards'

.png)

Inflation Steady, Home Sales Show Momentum

.jpg)

Weekend Talking Points - 'Counterintuitive?'

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.