.jpg)

Mortgage rates drifted higher on growing concerns that the Fed might NOT cut rates on September 17. Meanwhile, home price growth continues to moderate nationwide and transaction volumes remain stuck at roughly 4 million existing home sales per annum.

Fed minutes were pretty hawkish. The meeting notes from the last FOMC get-together on July 31 showed that (apart from the two dissenters) Fed members were much more worried about inflation than the jobs market. Combine that with today’s hawkish comments from voting Fed member Jeffrey Schmid, and you’ve got to be worried that Powell isn’t even going to greenlight a rate cut in September during his Jackson speech on Friday! [Federal Reserve]

TP: Keep in mind that the last FOMC meeting happened BEFORE the shocking revision of BLS jobs numbers. Nonetheless, due to the above, odds for a rate cut in September have dropped from 94% to 73% over the last two weeks.

Builders are bummed out. The National Association of Homebuilders’ confidence index dropped 1 point to 32 in August 2025. That’s low. Really low. To put that in perspective, the index was above 80 for most of the pandemic-driven construction boom (September 2020 — March 2022). Affordability concerns, tariffs, regulatory uncertainty, and rising vacancy rates are weighing on builder sentiment. [NAHB]

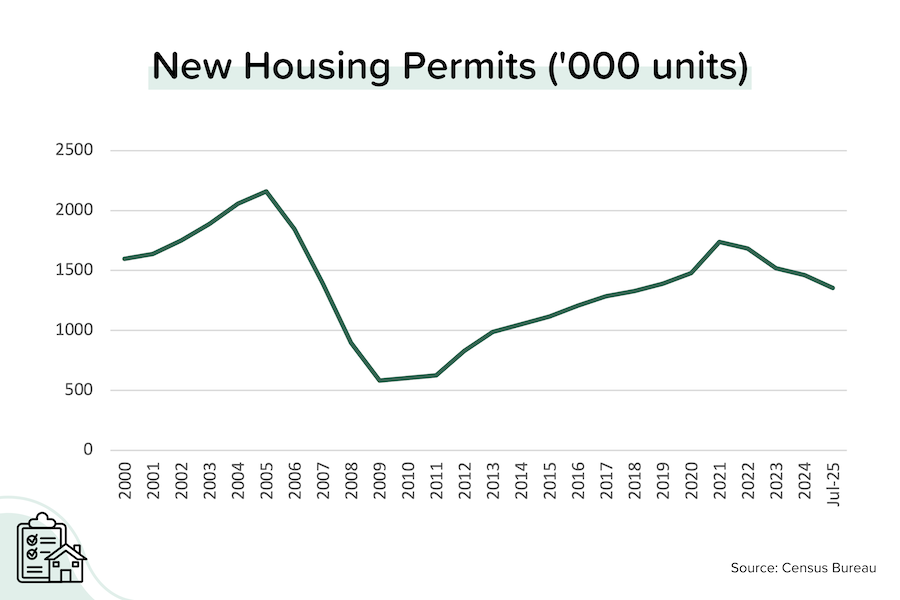

Mixed results from July housing starts. Permits for new units dropped 4% year-over-year to an annualized pace of 1.35 million units, 64% of which were for single-family homes. Housing starts, however, rebounded from several weak months to be up 8% YoY, with most of the growth coming from multifamily (>5 units) buildings. [Census Bureau]

TP: This report can be confusing, so here’s what’s important: 1) builders are pulling back on new MF projects given rising vacancy rates, 2) we seem unable to build much more than 1 million new SFHs a year, and 3) we need more (and more affordable) new homes to help us address our nationwide affordability issues (2–4 million unit shortage).

Rent growth slows. According to Zillow, national rent growth slowed to +2.6% YoY in July (from +2.9% YoY in June). In comparison, the rental index that the BLS uses rose +3.5% YoY, while the owner’s equivalent rent index rose +4.1% YoY. Why is that important? Because those two items represent ~41% of total “core” CPI. If the CPI utilized real-time “shelter” data instead (such as from Apartment List or Zillow), “core” CPI would be around +2.6% YoY rather than the reported +3.1% YoY. [Zillow]

TP: Around 56% of new home completions are in the South, putting pressure on rental rates. According to Zillow, rental rates are flat in Dallas, Las Vegas, and Orlando; and falling in Phoenix, San Antonio, Denver, and Dallas.

Prices fell in 39 of the Top 50 metros in July. At the nationwide level, prices were only down -0.1% month-over-month — hardly a crash — but this is the 3rd-straight month that Redfin’s national home price index has declined MoM. [Redfin]

TP: When we get the Case-Shiller numbers next week, I expect to see confirmation of these trends. Basically, nationwide prices are up ~2% YoY. But that represents the balance between half the country (South, Mountain regions) seeing price declines and the other half (Northeast, Midwest) seeing price increases.

As I have highlighted many times, the cities seeing the largest price declines today are (almost without exception) the ones where:

- Home price growth during the pandemic was extraordinary (40–80%)

- The inventory of existing homes is now well above pre-pandemic levels, and

- Builders ramped up new home/condo construction

Bond and Mortgage Market

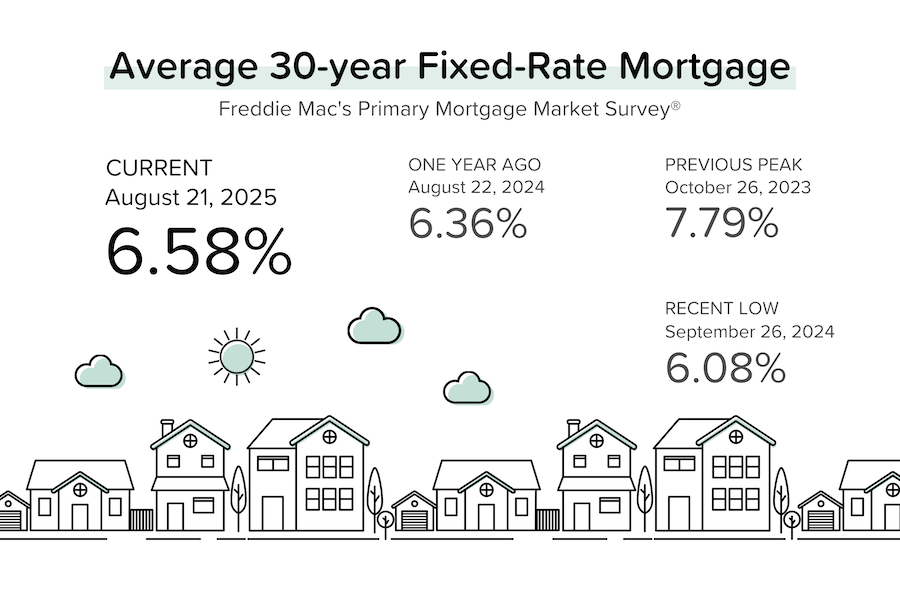

The market still expects a 25 basis point rate cut on September 17, but confidence is waning. Why? Wholesale inflation (PPI) appeared to be accelerating (tariffs?), combined with recent hawkish comments from various Fed members (discussed earlier).

The good news is average 30-year mortgage rates continue to hang near 6.5%. Part of the reason for this relative stability is that the “spread” between mortgage rates and US bond yields has been declining. That’s good news for borrowers. We’ve certainly seen a big pick up in consumer inquiries (coming from the Home Report) regarding refi opportunities.

Here are the current probabilities for Fed rate cuts at the next three meetings.

Note: The current Fed Funds Rate policy range is 4.25–4.50%.

- September 17 FOMC Meeting: A 73% probability that rates will be 25 bps below current (down big from 94% a week ago). 27% probability that rates will be unchanged.

- October 29 FOMC Meeting: 34% probability that rates will be 50 bps below current (down big from 63% a week ago). 51% probability that rates will be 25 bps below current (implying a rate cut in either September or October, but not both.)

- December 10 FOMC Meeting: 25% probability that rates will be 75 bps below current (down big from 53% last week). 47% probability that they’ll be 50 bps below current.

They Said It

“Housing affordability is central to the outlook for economic growth and inflation. Given a slowing housing market and other recent economic data, the Fed’s monetary policy committee should return to lowering the federal funds rate, which will reduce financing costs for housing construction and indirectly help mortgage interest rates.” — Robert Dietz, NAHB’s Chief Economist

“That last mile [to 2% inflation] is pretty hard. I think we got to be careful about what lowering short-term rates would do to the inflation mentality.” — Jeffrey Schmid, Kansas City Fed President

Related posts

.png)

Inflation Below Forecasts, Home Sales Rise

.jpg)

Weekend Talking Points - 'Treat'

.png)

Home Builder Confidence Hits 6-Month High

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.