.jpg)

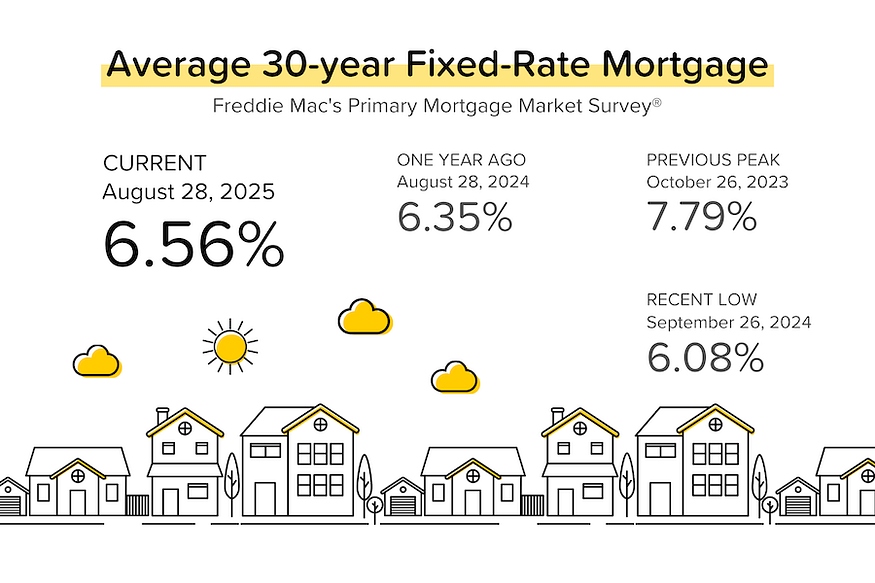

The last week has been momentous, with Jerome Powell signaling rate cuts ahead, average 30-yr mortgage rates falling to near 6.50%, and national home prices declining for the fourth-straight month (on a seasonally-adjusted basis).

Powell greenlights rate cuts at Jackson Hole. As usual, the Fed Chair’s message was subtle. But it was also unambiguous: “the shifting balance of risks may warrant adjusting our policy stance.” By the “balance of risks”, he meant weighing the risks of higher inflation (from tariffs) vs. the risks of higher unemployment (given the recent shocking revisions to the BLS jobs report).

“Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.” — Jerome Powell, Federal Reserve Chairman

Bond markets rejoiced. The yield on the 10-year US treasury bond dropped 6 basis points to 4.26% on the day, and average 30-year mortgage rates dropped from 6.62% to 6.52%. The fed funds rate futures market is now pricing in an 85% probability of a 25 basis point rate cut on September 19. [Source: MBS Highway, CME]

Trump goes after Cook. President Trump announced on social media that he was “firing” Fed Governor Lisa Cook over alleged “mortgage fraud”. Does he have the authority to do that? Does he care that the answer is probably ‘no’?

TP: The President is doing everything he can to stack the deck with dovish supporters, but Fed independence shouldn’t be trifled with.

Existing home sales stay stuck. I feel like I’ve been saying this for years — oh, because I have. July 2025 existing home sales rose 2.0% month-over-month to 4.01 million units. The median listing price fell 2.4% MoM to $422K, as total inventory (this includes homes already under contract) rose to 1.55 million, the highest level since November 2019. [Source: NAR]

TP: In 2019, 5.3 million existing homes changed hands. In 2025, it looks like around 4.0 million will do so. Same Inventory level (1.5 million) + slower Existing Home Sales pace = rising Days on Market.

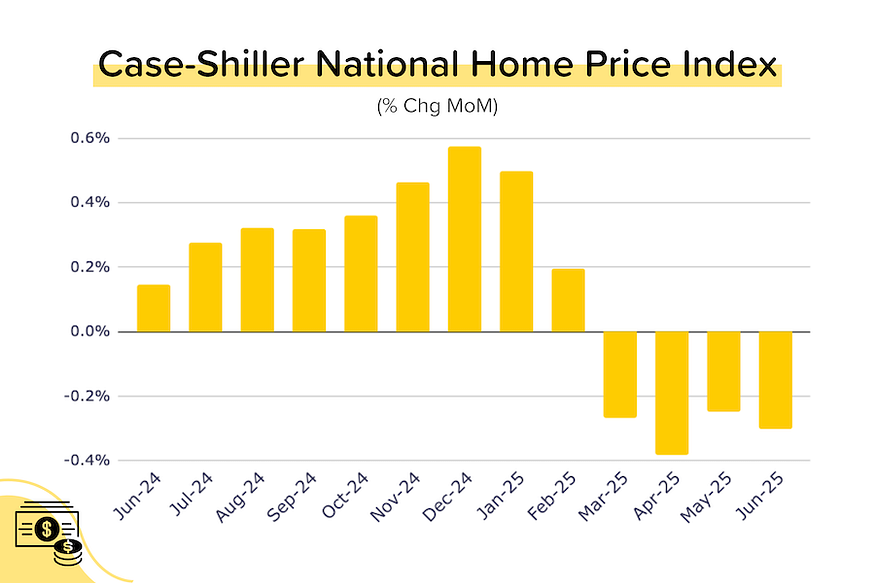

Case-Shiller index saw further declines. In June 2025, Case-Shiller’s seasonally-adjusted national home price index declined 0.3% MoM. That was the 4th-straight monthly drop in the SA index. (It should be noted that on an unadjusted or ‘raw’ basis, home prices rose ever so slightly MoM.) 17 of the 20 big city SA indexes also saw MoM declines, and 7 of them are down year-over-year as well. [More on this later]

On the Case (Shiller) in June 2025

Annual price growth for Case-Shiller’s seasonally-adjusted national index decelerated to just +1.9% YoY in June 2025. (We started the year at +4.1% YoY!) June 2025 also marked the 4th-straight month of MoM declines in the index. Annualize the last 6 months of data and you get -0.9%. Annualize the last 3 months and you get -3.6%. Basically prices are running flat to down except for some major cities in the Northeast and Midwest.

As we do each month, we looked at the 20 big city indexes in detail. Here’s what we found:

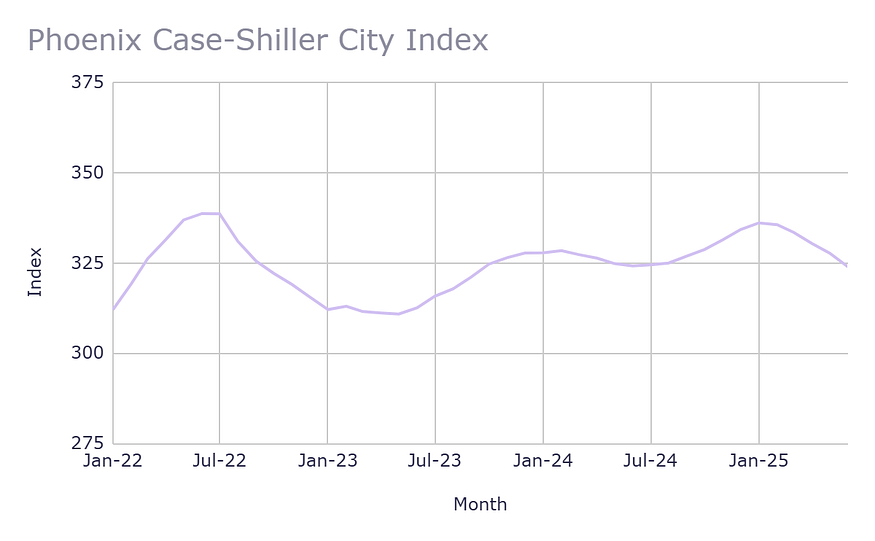

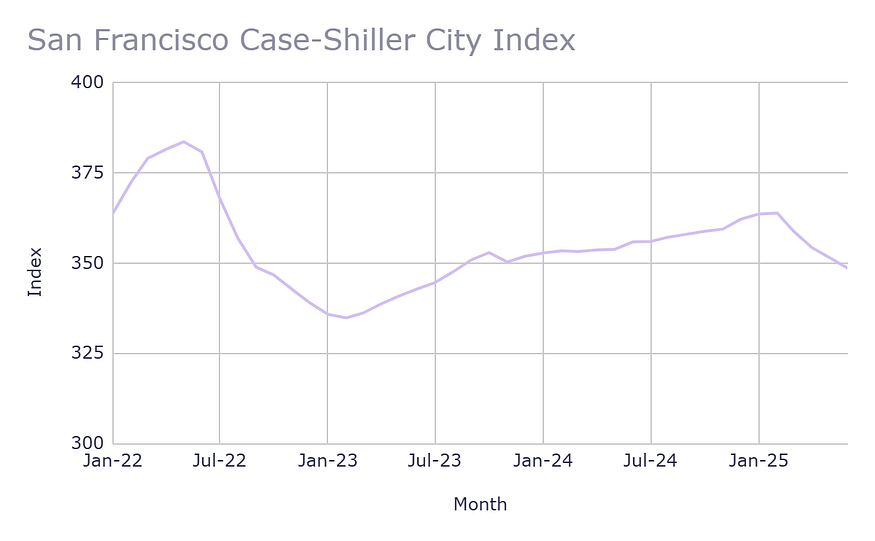

- 17 of the 20 big city indexes saw their SA indexes decline MoM in May (up from 12 last month): The largest drops were seen in Phoenix (-1.2% MoM), San Francisco (-0.8% MoM), Miami (-0.8% MoM) and Washington D.C. (-0.6% MoM).

- The biggest MoM increases came from New York and Chicago (both pretty modest at +0.2% MoM). The highest annual growth also came from New York City (+7.0% YoY) and Chicago (+6.1% YoY).

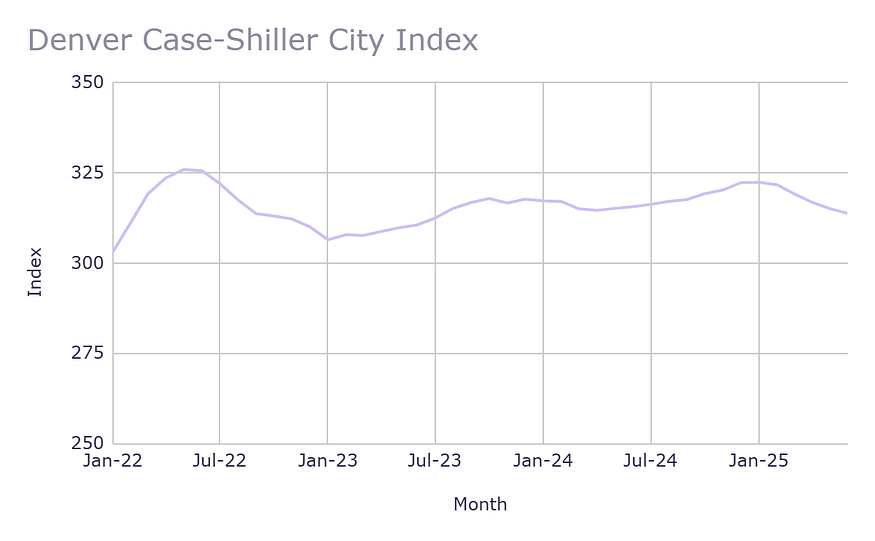

- 7 of the 20 big cities are now seeing YoY price declines in their SA indexes (from 4 last month): San Diego (-0.7% YoY), Miami (-0.3% YoY) and Phoenix (-0.1% YoY) joined Tampa (-2.4% YoY), San Francisco (-2.1% YoY), Dallas (-1.0% YoY) and Denver (-0.6%). These declines are still tiny compared to their pandemic-era price gains, but the trajectory is telling.

- Only two cities are still making all-time highs: That’s right — NYC and Chicago.

Reminder: The Case-Shiller index is the gold standard for measuring home price growth because it uses the repeat sales method (looking at ‘pairs’ of transactions for the same home) to more accurately gauge true appreciation. However, this accuracy comes at a cost: a nearly two-month time lag.

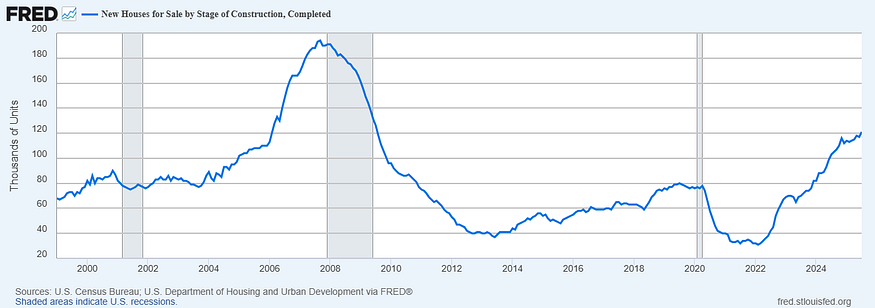

Lots of new homes for sale too.

On the surface, the new home sales figure for July 2025 (652K annualized) wasn’t terribly exciting. But it was intriguing to see the inventory of new homes for sale rise 7.3% to 499K units. Of that 499K for sale, 121K (about 24%) were already completed. That 121K is the highest figure we’ve seen since August 2009. That’s 2.2 months’ worth of sales, just sitting there.

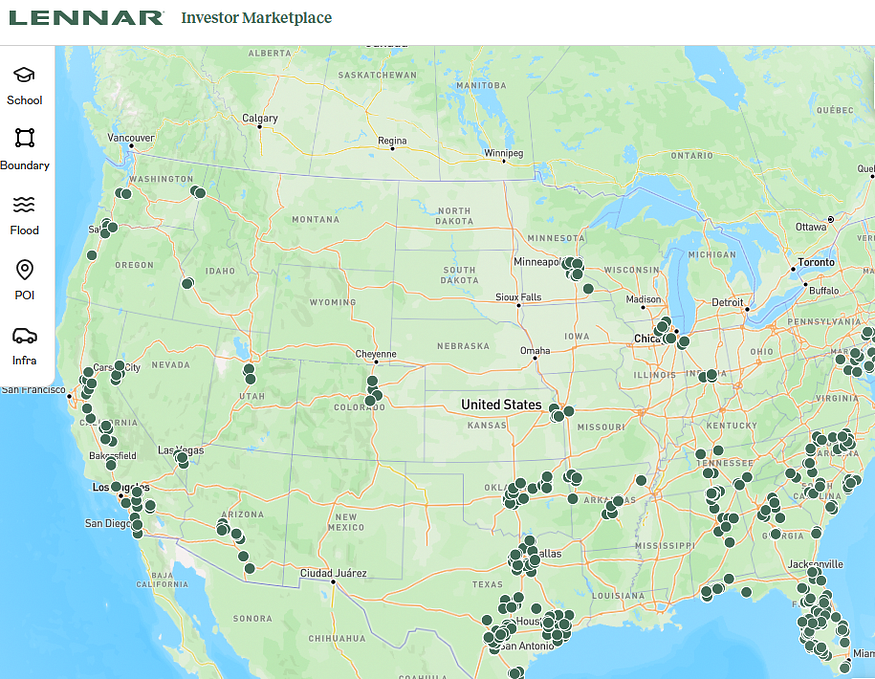

It’s no coincidence that Lennar (one of the nation’s biggest builders) just launched a very impressive site — Investor Marketplace — allowing them to sell new homes (with bundled financing) directly to mom-and-pop landlords. You can even screen by capitalization rate and potential ROI!

Here’s another interesting little fact: with builders retooling plans and building smaller homes, the median price of new homes sold in July was $404K. That’s 4% cheaper than the median price of existing homes sold ($422K). New homes cheaper than old homes? And…builders can offer attractive rate buy-down financing packages.

Bond and Mortgage Market

Powell’s Jackson Hole speech increased market confidence that the first rate cut of 2025 will come on September 17. But the odds of further rate cuts in October and December didn’t really change that much. With the risks to inflation (upside) and employment (downside) currently “balanced” according to Jerome Powell, additional rate cuts will ultimately depend on the data: we’ve got several inflation and jobs reports before year-end.

Note: The current Fed Funds Rate policy range is 4.25–4.50%.

- September 17 FOMC Meeting: A 85% probability that rates will be 25 bps below current (up from 73% a week ago). 15% probability that rates will be unchanged.

- October 29 FOMC Meeting: 44% probability that rates will be 50 bps below current (up from 34% a week ago). 49% probability that rates will be 25 bps below current (implying a rate cut in either September or October, but not both.)

- December 10 FOMC Meeting: 36% probability that rates will be 75 bps below current (up from 25% last week). 48% probability that they’ll be 50 bps below current.

They Said It

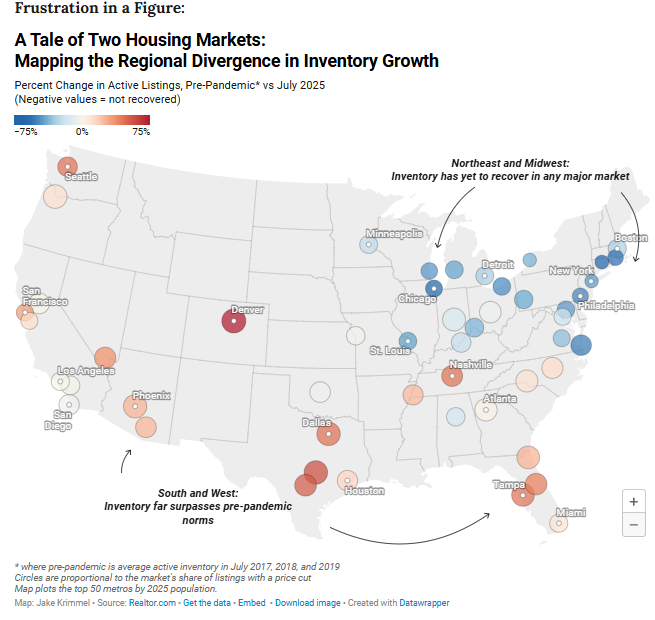

“Geographically, this summer’s housing market looks like two different countries stuck together. In the South and West, there’s a glut of inventory and very little demand, thanks to the pandemic-era price boom and higher interest rates. In the Northeast and Midwest, it’s almost the polar opposite: Homes are in short supply, and demand remains quite resilient. Homes in the Midwest and Northeast are actually selling, respectively, 1 and 2 weeks faster than they were before the pandemic, despite those same high mortgage rates and still-climbing prices.” — Jake Krimmel, Realtor.com Economist

Related posts

.png)

Inflation Below Forecasts, Home Sales Rise

.jpg)

Weekend Talking Points - 'Treat'

.png)

Home Builder Confidence Hits 6-Month High

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.