.jpg)

There were many encouraging signs for the housing market this week: lower mortgage rates are boosting demand for new and existing homes, December CPI (inflation) came in lower than expected, and President Trump unveiled a number of (rough) plans to improve affordability.

Mortgage rates remained in the low 6% range. Average 30-year mortgage rates have been below 6.25% for a month, and below 6.50% for nearly 5 months. That’s giving would-be buyers the time they need to locate, inspect and negotiate on their next home. [Freddie Mac]

New home sales for October were up big. We finally got the long-delayed October new home sales figures from the Census Bureau, and they were up 19% year-over-year to 737,000 homes (seasonally-adjusted, annualized rate). The September number was 738,000. We haven’t seen new home sales running at this pace since May 2023! The median price of the new homes sold was $392,300, down 8% YoY. But this was mainly due to the mix of homes for sale. In October 2025, 54% of homes for sale were priced <$400,000. In October 2024, that was only 43%. [Census Bureau]

Existing home sales for December were up big too. Existing home sales rose 5.1% month-over-month to 4,350,000, the fastest pace of sales since March 2023. The total inventory of homes for sale plunged (as it always does this time of year) to 1,180,000, and the median sales price was roughly flat YoY at $405,400. [NAR]

TP: Are we finally breaking free of the 4 million unit pace we’ve been stuck at for the past 2.5 years? It looks that way!

MBS Highway Housing Survey for January. The MBS Highway National Housing Index saw a solid rebound in January 2026, rising 7 points from December to 34. A year ago, the index stood at 36. Lower mortgage rates are beginning to support transaction activity and put modest upward pressure on prices. [MBS Highway]

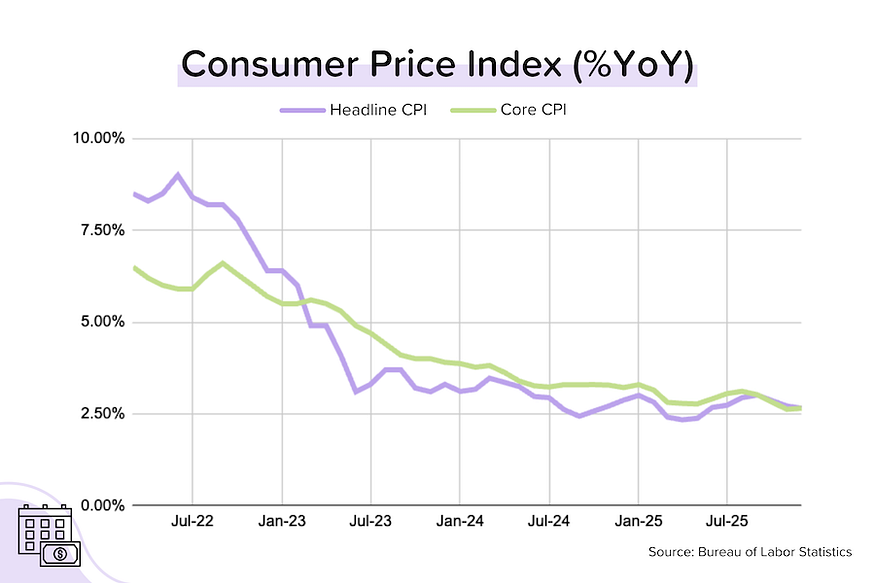

December “core” CPI came in lower than expected. “Core” CPI (inflation) rose +0.2% MoM and +2.6% YoY in December 2025 (lower than the +2.7% YoY expected). [BLS]

Bond and Mortgage Market

After President Trump instructed the GSEs (Fannie and Freddie) to buy (over time) up to $200B in Mortgage Backed Securities, average 30-year mortgage rates have moved into the (very) low 6% range. Despite this, market expectations are that the Fed will NOT cut rates at either of the next two meetings.

Note: After the rate cut on Dec 10, the Fed Funds Rate policy range is now 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- January 28 FOMC Meeting: 95% probability that the Fed does nothing (was 88% last week); only a 5% probability of a 25 bps rate cut.

- March 18 FOMC Meeting: 78% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was 59% a week ago). In other words, no cut at either the January or March FOMC meetings. Only a 22% probability that rates are 25 bps below current (was 41% last week), which would imply a 25 bps rate cut at the March 18 meeting.

They Said It

“2025 was another tough year for homebuyers, marked by record-high home prices and historically low home sales. However, in the fourth quarter, conditions began improving, with lower mortgage rates and slower home price growth. December home sales, after adjusting for seasonal factors, were the strongest in nearly three years. The gains were broad-based, with all four major regions improving from the prior month.” — Lawrence Yun, NAR’s Chief Economist

“Late last week, mortgage rates dropped, driving the weekly average down to its lowest level in more than three years. The impacts are noticeable, as weekly purchase applications and refinance activity have jumped, underscoring the benefits for both buyers and current owners. It appears that housing activity is improving and poised for a solid spring sales season.” — Freddie Mac PMMS Survey

Related posts

Home Price Forecasts Signal Opportunities Ahead

.jpg)

Weekend Talking Points - 'High Fives'

FAQ: Why would I ever give up my low mortgage rate?

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.