CPI was steady in February. “Core” CPI (Consumer Price Index = inflation for you and me) was flat in February at 2.5% year-over-year. Flat is ok. But we’re no closer to the Federal Reserve’s 2% inflation goal, and the March CPI will almost certainly move higher due to the spike in oil prices. Brent crude was priced at $72/barrel on Feb 27; today it’s nearly $95/barrel. [BLS]

Existing home sales grew, but remained low. In February, existing home sales rose 1.7% month-over-month (-1.4% year-over-year) to 4.09 million units (SAAR). While that beat Wall Street Expectations, it wasn’t terribly exciting. We’ve been stuck at around 4 million units for more than three years.

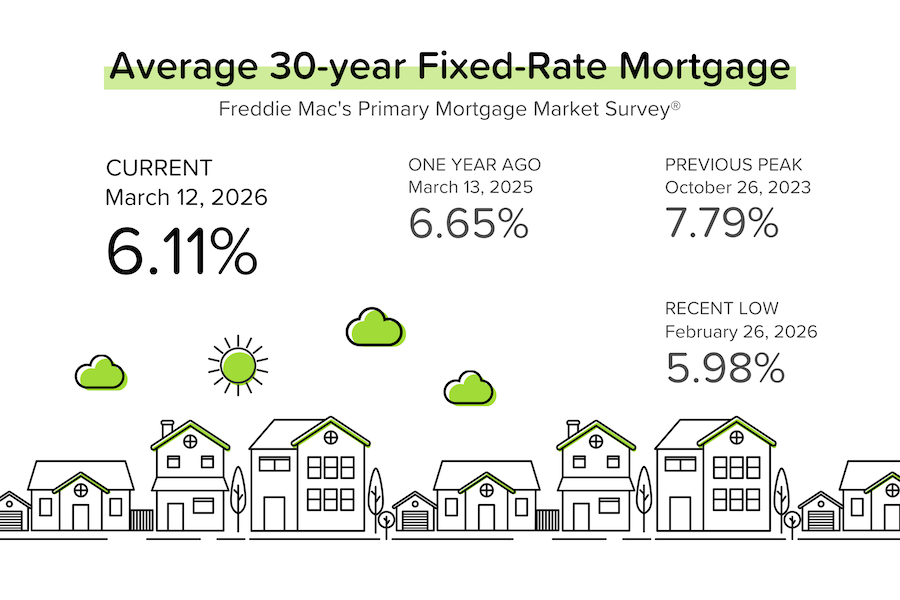

TP: It is concerning that the fall in mortgage rates over the course of 2025 has not translated into a significant boost in transaction volumes — at least not yet. As a reminder, in October 2023 (when average mortgage rates briefly exceeded 8%), we got existing home sales of 3.8–3.9 million units (SAAR). Today, we’re only getting 4.1 million, despite rates in the low 6% range (that’s -200 bps) and with 15% more homes for sale!

But real estate agents are getting pretty bulled-up. According to the Realtors Confidence Index for March 2026, 37% of agents expected a YoY increase in buyer traffic over the next 3 months. That’s the highest figure we’ve seen for that since February 2022. In addition, 31% of agents expected an increase in seller traffic over the next 3 months. That’s the highest figure since June 2021.

TP: What’s driving this increased optimism? Lower mortgage rates everywhere + lower home prices in many metros = improved affordability.

Oil prices keep rising. Oil fuels the global economy, literally. With the conflict in Iran effectively stopping the critical flow of oil & gas tankers through the Strait of Hormuz, global oil prices have spiked (because supply is constrained). Brent crude prices have risen from $72 pre-conflict to nearly $95 today (+32%). That is already having an impact on inflation, and rising inflation is bad for bonds and, by extension, mortgage rates.

TP: The last thing we need just before spring selling season kicks off is a surge in mortgage rates. While mortgage rates have moved up from their recent lows of 5.99%, they still remain in the low 6% range.

Solid new home starts — led by multifamily. In January, housing starts rose 7.2% MoM (+9.5% YoY) to 1.49 million units (SAAR). That’s the strongest figure we’ve seen since February 2025, and it was driven by a resurgence in multifamily (condos, townhomes etc.) construction. MF starts jumped 29% MoM and 57% YoY.

TP: As you know, a lot of the oversupply (in many markets) has been in the MF space. Apartment vacancy rates have been at record levels and rental rates have been under pressure for more than 2 years. Is this the first sign that MF absorption is picking up? We’ll have to see what happens in February, because this data series is historically quite volatile.

Bond and Mortgage Market

Is the oil getting through the Strait of Hormuz? Are Persian Gulf producers slowing production because their terminals are filling up? The bond market has been fixated on the flow of fuel, with oil prices staying elevated despite: 1) Trump’s assurance that tankers would be both protected and insured, and 2) the IEA’s decision for a coordinated release of 400 million barrels from global strategic petroleum reserves.

So why isn’t this leading to lower oil prices? If you haven’t read Robert Kaplan’s “The Revenge of Geography”, I suggest you do, especially the chapter on Iran — the only country that spans the Greater Middle East’s two most important petrochemical production areas: the Persian Gulf and the Caspian Sea. Geography itself grants Iran significant leverage.

With the world focussed on Iran and oil prices, nobody is paying much attention to the latest US inflation statistics, which cover the period before the conflict started. If the war continues for several months, inflation will rise, and that’s bad for bonds and, by extension, mortgage rates.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- March 18 FOMC Meeting: 99% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was 97% a week ago). The market thinks there is NO WAY the Fed will cut rates at this meeting. With oil prices up so much, that’s no surprise.

- April 29 FOMC Meeting: 93% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was 87% last week). In other words, no rate cut at EITHER the March or April FOMC meetings.

- June 17 FOMC Meeting: 77% probability that the Fed Funds rate will be kept at 3.50–3.75% (was 67% last week). That means that the odds are there will be no Fed rate cut for three straight FOMC meetings.

They Said It

“Housing affordability is improving, and consumers are responding. Still, there is a long way to go to return to pre-pandemic levels of transaction activity. There are more than 6 million more jobs than in 2019, yet home sales per year are down by one million. Despite the modest gain in home sales, actual housing demand remains muted relative to wage growth and job gains. Inventory is growing, but sluggishly.” — Lawrence Yun, NAR’s Chief Economist

Related posts

FAQ: Do global events affect mortgage rates?

.png)

Pending Home Sales Rise, Retail Sales Surprise

FAQ: What home price is right for me?

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.