.jpg)

So far, there has been nothing from “jobs week” to derail a Fed rate cut on September 17. In fact, the jobs data has generally come in weaker than expected. At the same time, a growing number of Fed members are voicing concerns about the upside risks to the unemployment rate.

Appeals court says Trump’s tariffs are illegal. The court ruled that President Trump had unlawfully used the International Emergency Economic Powers Act (IEEPA) as justification for his global, ‘reciprocal’ tariffs. The case will head to the Supreme Court next. If the SCOTUS upholds the appeals court ruling, the US could find it needs to refund billions of dollars.

TP: Under the Constitution, Congress has the power to set tariffs and regulate trade with other countries. But…there are various Acts that delegated power to the President to set tariffs (without getting Congress’ approval) in certain cases, such as ‘unfair trading practices’.

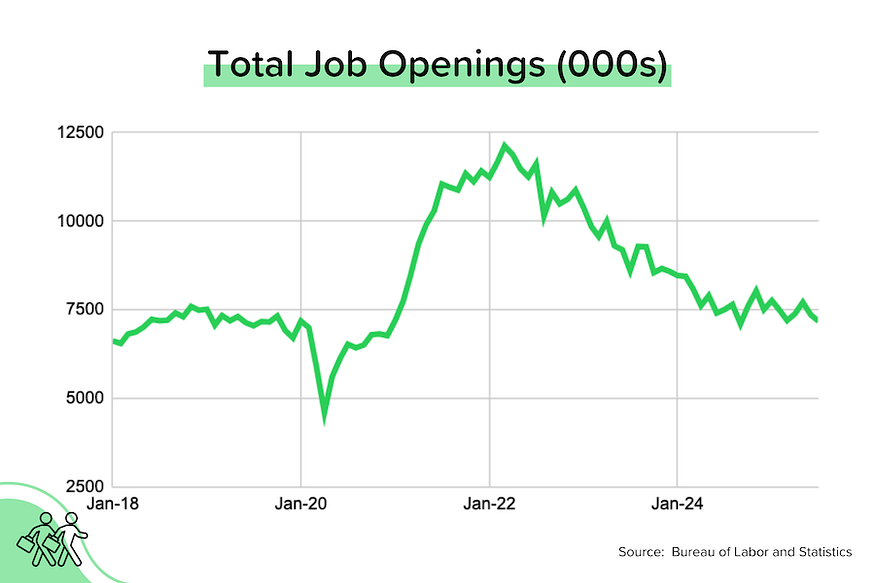

Job openings dropped. The latest JOLTS report (Job Openings & Labor Turnover Survey) showed that total job openings in July 2025 fell 2% month-over-month to 7.18 million. That was below expectations (~7.4 million), and is the lowest figure seen since December 2020. Both the hires rate (3.3%) and the quits rate (2.0%) remained very low.

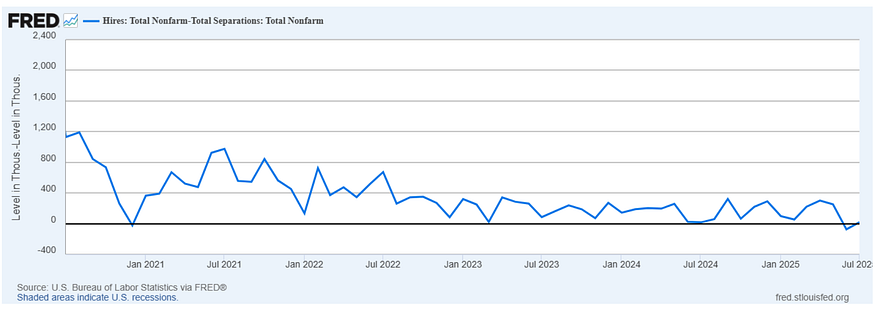

TP: It doesn’t get mentioned a lot, but the JOLTS report also provides a figure for the actual number of hires vs. separations (quits + layoffs). In July 2025, the number of net hires (hires minus separations) was just 19,000. And the revised figure for June 2025 was -74,000. While this figure does not tie directly with the BLS jobs report, it is noteworthy how low/negative this net hires figure has been lately (see graph below).

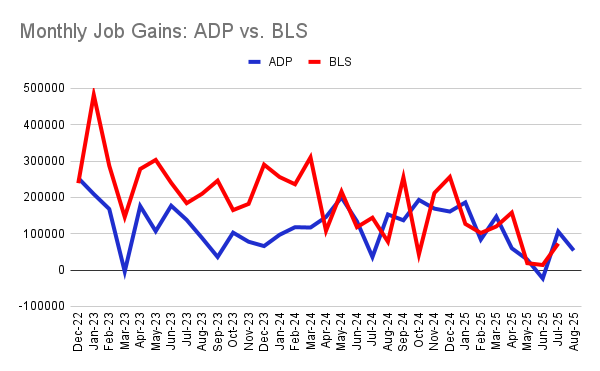

ADP: Weak private job growth. Private employers added just 54,000 jobs in August (vs. 70,000 expected). Over the last six months, job gains have averaged 62,000 per month. Over the last 3 months, 46,000. The annual wage increase for “job leavers” was 7.1%, while the increase for job stayers was 4.4%.

TP: 4 of the 10 industries tracked by ADP saw net job losses (manufacturing, trade & transportation, financial activities and education & health services). If not for a chunky 50,000 job gain from the leisure & hospitality sector, overall job growth would have been near zero.

A Challenging job market. In August, companies announced 85,979 job cuts. That was up 39% month-over-month and 13% year-over-year. It was also the worst August for announced job cuts since 2020 (COVID). And if you treat 2020 as an outlier, it’s the worst August since 2008. At the same time, employers announced plans to add just 1,500 jobs in August. That was the lowest total for August since Challenger started tracking the data.

TP: The Challenger jobs report looks at announced hiring and firing plans. So it’s meant to be forward-looking. If so, the future isn’t looking great for people looking to find/keep a job.

BLS jobs report out on Friday (today). Wall Street economists are looking for 75,000 job gains in August and for the unemployment rate to tick up to 4.3% (from 4.2% in July). The market will also be (unusually) focused on the revisions to the prior months. As a reminder, when the July BLS report came out, the jobs numbers for May and June were revised down by a combined 258,000 jobs.

TP: Things could get really interesting here. After Trump fired the previous BLS Commissioner and replaced her with EJ Antoni, the market has become very concerned that the ‘believability’ of the BLS numbers could suffer. This is ironic, of course, since we’ve been questioning the believability of the BLS numbers for years. Whatever numbers we get on Friday, everything will be viewed through a political lens. Personally, I hope that the BLS: 1) delays the publication of the report by a couple of weeks to get a more accurate initial reading, and 2) makes responding to the survey mandatory.

The 40-Year Old (Homebuying) Virgin

The NAR reported that in 2024, the median age of first-time homebuyers shot up to 38 years old. Think about that for a minute! People are graduating from college, and then waiting 14 years before they buy their first home?

There are a number of contributing factors to this (people getting married later, people having kids later, etc.) but affordability is clearly the primary issue. The rise in home prices during the pandemic, combined with higher mortgage rates starting in 2022, has put homeownership out of reach for many younger Americans.

There’s another (statistical) wrinkle here. If younger first-time buyers can’t get involved, that guarantees that the median age of first-time buyers will rise. It doesn’t mean that younger first-time buyers want to delay buying a home. They just can’t manage it financially. But as affordability improves (lower home prices in many markets, mortgage rates moving below 6.50%), those younger first-timers will take the plunge, and the median age will drop again.

So I’m not discouraged by the median age of first-time home buyers rising from 33 (2020) to 38 (2024) in the wake of the pandemic. I think it shows just how out-of-whack the market is right now, and how much upside there is to transaction volumes when affordability improves. We might end up with a similar figure for 2025, but I’m pretty confident that we’ll be back to the low 30s by 2027.

Bond and Mortgage Market

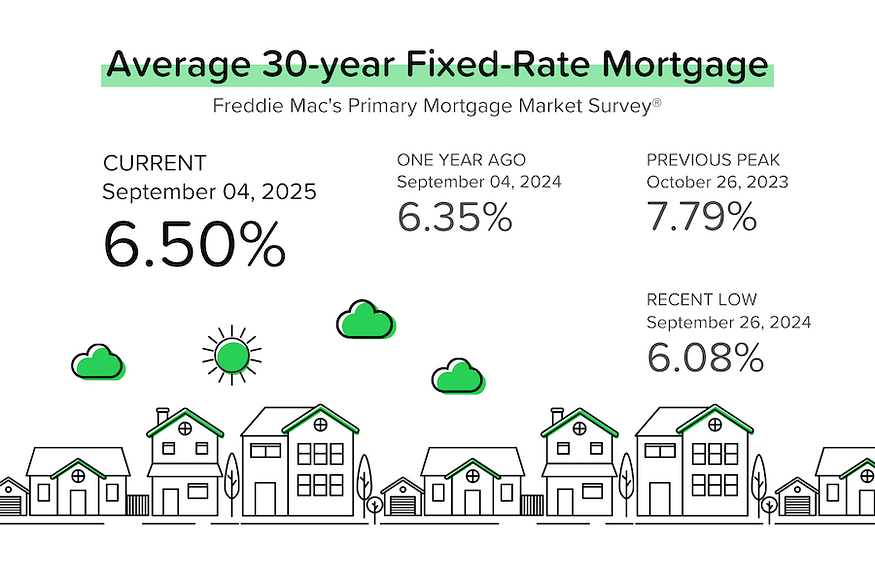

“Jobs week” has so far been supportive of higher bond prices and lower bond yields. The JOLTs report showed a sizable drop in job openings, ADP reported very modest job gains, and the Challenger report highlighted rising job cut announcements. The yield on the 10-year US treasury is currently trading just below 4.20%, and average 30-year mortgage rates have moved to 6.5%.

With all of the above in mind, it’s no surprise to see that the probabilities for rate cuts have risen. A rate cut in September is fully priced-in. Beyond that, the market is still uncertain if we’ll get 1 or 2 more rate cuts before year-end.

Note: The current Fed Funds Rate policy range is 4.25–4.50%.

- September 17 FOMC Meeting: 97% probability of a 25 bps rate cut (up from 85% a week ago).

- October 29 FOMC Meeting: 54% probability that rates will be 50 bps below current (up from 44% a week ago). That means a 25 bps rate cut at both the September and October meetings. 45% probability that rates will be 25 bps below current (implying a rate cut in either September or October, but not both).

- December 10 FOMC Meeting: 45% probability that rates will be 75 bps below current (up from 36% last week). That means a rate cut at each of the three meetings before year-end. 46% probability that they’ll be 50 bps below current.

They Said It

“The year started with strong job growth, but that momentum has been whipsawed by uncertainty. A variety of things could explain the hiring slowdown, including labor shortages, skittish consumers, and AI disruptions.” — Nela Richardson, ADP’s Chief Economist

“After the impact of DOGE on the Federal Government, employers are citing economic and market factors as the driver of layoffs. We’ve also seen a spike in cuts due to operation or store closings and bankruptcies this year compared to last.” — Andrew Challenger, Senior Vice President for Challenger, Gray & Christmas.

Related posts

.png)

Inflation Below Forecasts, Home Sales Rise

.jpg)

Weekend Talking Points - 'Treat'

.png)

Home Builder Confidence Hits 6-Month High

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.