.jpg)

Last week, the market decided it didn’t believe the strong January BLS jobs report — especially not in light of the huge revisions to the full-year 2025 numbers. Then on Friday we got a big drop in the January CPI (inflation). Net result: US treasury yields moved sharply lower and mortgage rates followed.

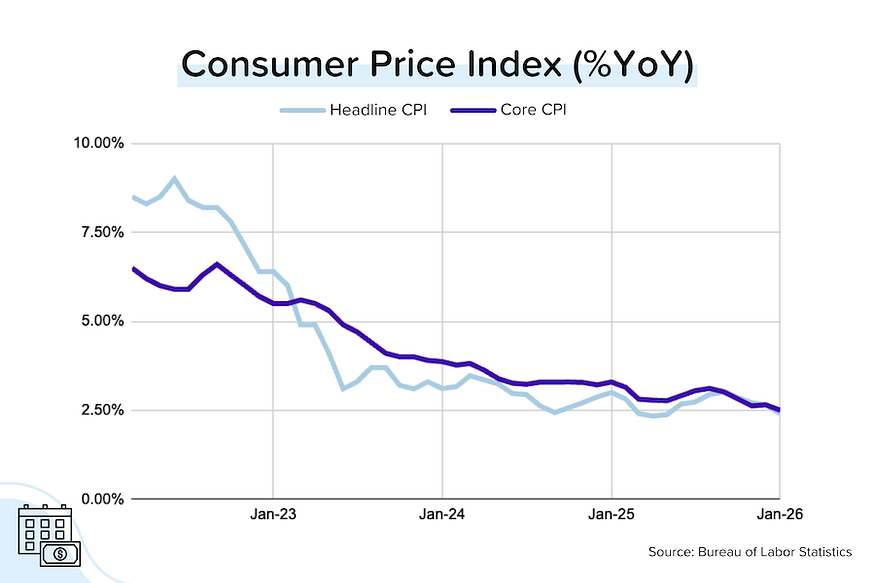

January CPI moved much lower. Headline CPI (Consumer Price Index = inflation for you and me) dropped to +2.4% YoY (from +2.7%), and “core” eased to +2.5% YoY (from +2.7%). That’s the lowest “core” reading we’ve had since March 2021. [BLS]

TP: Remember, a lower rate of inflation DOES NOT mean that prices are falling. It just means that prices are growing at a slower pace. The Federal Reserve is comfortable with 2% “core” inflation per year — it is NOT attempting to stop inflation and definitely doesn’t want deflation.

Treasury yields and mortgage rates responded. The yield on the 10-year US treasury bond plunged from 4.18% to 4.05%, and the average 30-year mortgage rate dropped from 6.14% to 6.04% — essentially at a 3-year low. [MBS Highway, Mortgage News Daily]

TP: Inflation eats away at the real returns from holding fixed-income securities like US treasury bonds. So when inflation moves down, bond prices tend to rise. Mathematically, when bond prices rise, bond yields fall. And mortgage rates tend to follow movements in bond yields, especially the yields on mortgage backed securities (MBS).

Rents continue to decline YoY. The nationwide median asking rent was down 1.5% year-over-year in January 2026, the 29th-straight month of declines. Rents are now 4.8% below their mid-2022 peak. The national vacancy rate stands at 7.6% — well above the pre-pandemic average of 6.9%. [Realtor.com]

Priciest global housing markets. Nine of the 20 least affordable cities in the world are in the USA, and six of those in California, including the #1 least affordable city — San Jose. Other unaffordable US markets? LA, NYC, Miami, San Francisco, Oakland, Boston, San Diego and Long Beach. The least affordable foreign market? Vancouver, Canada. [Realtor.com]

Still working through the last construction boom. We finally got the delayed new home starts and permits data from the Census Bureau. Probably the most interesting detail from the report was the continued decline in homes “Under Construction”, which fell to an annualized pace of 1.28 million units — the lowest since January 2021. [Census Bureau]

TP: The boom in permits in 2021 (1.74 million) and 2022 (1.68 million) is still being felt in elevated “Completions” today, but builders aren’t ‘re-upping’ permits at the same pace, despite the much-publicized housing shortage.

Pending sales were disappointing — again. NAR’s Pending Home Sales Index (“PHSI”) fell 0.8% month-over-month in January 2026. That followed a 7.4% MoM drop in December 2025. The January 2026 PHSI index figure of 70.9 is the lowest in the index’s history — which is very strange considering that average 30-yr mortgage rates are near 6%. [NAR]

TP: Weather played a big impact in this weak PHSI figure. It’s notable that the two regions hit hardest by the snow/cold snap in January were the Northeast (-5.7% MoM) and South (PHSI -4.5% MoM), while the less affected Midwest (+5.0% MoM) and West (+4.3% MoM) saw solid growth. As the chart above shows, it is very unusual for mortgage rates to be this low and PHSI to also be low. I’m convinced that we’ll see a snapback soon.

Bond and Mortgage Market

When the January BLS jobs report came out last Wednesday (jobs +130K, way ahead of expectations), the initial market reaction was sharply negative — as you’d expect. But as the day progressed, and more people started commenting on the massive revisions to the full-year 2025 figures, skepticism began to grow, and the bond market damage was contained. Then, on Friday, the “core” CPI for January came in at +2.5% YoY, the lowest pace of inflation seen since March 2021.

The net result was that 10-year US treasury yields dropped from 4.18% to as low as 4.04%. The yield on mortgage backed securities (a key driver of mortgage rates) didn’t fall as much, but mortgage rates still moved tantalizingly close to 6%. The latest Freddie Mac PMMS survey showed that average 30-year mortgage rates had dropped to 6.01% — the lowest level since September 2022.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- March 18 FOMC Meeting: 94% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was also 94% a week ago). In other words, no rate cut at the March FOMC meetings.

- April 29 FOMC Meeting: 79% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was also 79% last week). In other words, no rate cut at EITHER the March or April meeting. 21% probability that rates will be 25 basis points below current (was also 21% last week), which implies a 25 bps rate at the April meeting.

They Said It

“Improving affordability conditions have yet to induce more buying activity. With mortgage rates nearing 6%, an additional 5.5 million households that could not qualify for a mortgage one year ago would qualify at today’s lower rates. Most newly qualifying households do not act immediately, but based on past experience, about 10% could enter the market — potentially adding roughly 550,000 new homebuyers this year compared with last year.” — Lawrence Yun, NAR’s Chief Economist, discussing the January 2026 PHSI

“Housing affordability remains an ongoing challenge at the start of 2026. The solution for the housing market is the enactment of policies that will bend the construction cost curve and enable additional supply of attainable housing. On the positive side, easing inflation should continue to allow lower interest rates for mortgages and builder loans.” — Robert Dietz, NAHB’s Chief Economist

Related posts

April 2026 MBS Highway Housing Index

.png)

Energy Prices Push Inflation Higher

.jpg)

Weekend Talking Points - 'Ceasefire'

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.