.png)

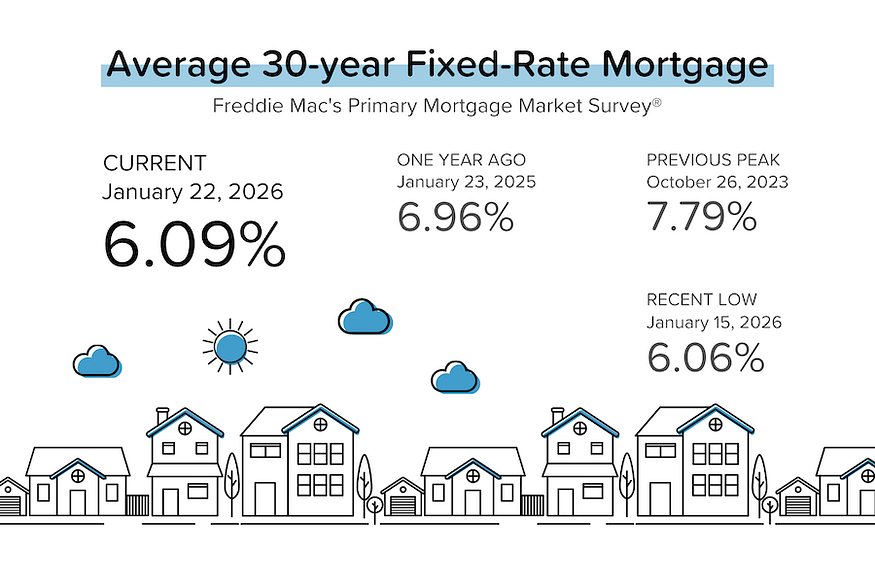

December and January are two of the slowest months of the year for home sales. But the spring selling season is around the corner (things really start perking up in March), and if mortgage rates can stay in the low 6% range, activity levels should surge.

Pending sales cratered in December. It doesn’t make a lot of sense. Average 30-year mortgage rates remained below 6.25% in December 2025, but NAR’s Pending Home Sales Index (“PSHI”) dropped 9.5% month-over-month to 71.8? A year ago, average 30-yr mortgage rates were at 7%, but the PHSI in December 2024 was 3% higher than in December 2025? A PSHI level of 71.8 suggests that the annualized pace of existing home sales has dropped back below 4 million units. [NAR]

TP: December typically has the lowest “raw” (not seasonally-adjusted) PHSI of the year. With cold weather and the kids in school, both the number of listings and the number of transactions are at/near their lows. So changes in seasonal-adjustment factors can skew the numbers. But there’s still something strange about this result. By the way, the Midwest’s regional index fell 14.9% — to a level we haven’t seen in years. Very odd, indeed. I expect a snapback in January.

Similar January disappointment for builders. Average 30-year mortgage rates got as low as 6.06% in early January, yet the National Association of Homebuilders’ confidence index still fell 2 points month-over-month to 37.

“While the upper end of the housing market is holding steady, affordability conditions are taking a toll on the lower and mid-range sectors. Buyers are concerned about high home prices and mortgage rates, with down payments particularly challenging given elevated price to income ratios.” — Buddy Hughes, NAHB’s Chairman

Despite new homes being cheaper than existing homes. Strange, but (statistically) true: the median new home price ($392K in October according to the Census Bureau) was lower than the median sales price of an existing home ($415K in October according to the NAR). That’s certainly attention-grabbing (why would anyone pay more for an older home?) but it’s not an apples-to-apples comparison. As we’ve highlighted previously, builders have been constructing smaller homes to keep the prices down. And 60–70% of new home sales are in the (more affordable) South, while only 45% of existing home sales are in the South.

Trump talked housing affordability in Davos. An ultra-exclusive conference of billionaires, politicians, NGOs and celebrities seemed an odd place for President Trump to discuss his plans to reinvigorate the American Dream of homeownership. Or perhaps it’s brilliant, since there was no shortage of big bank and big investor CEOs in Switzerland, and President Trump wants more/cheaper lending for would-be buyers and to keep Blackrock from buying every home on your block.

TP: Here’s the thing: he’s not actually banning Blackrock from buying homes, he’s just limiting the ability of big institutions to get access to conventional lending. Essentially, Fannie Mae and Freddie Mac have been told to stop guaranteeing mortgages for SFH purchases made by large institutional investors. But…Blackrock can still buy SFHs using all-cash…and the definition of what a large institutional investor has yet to be set.

Here’s what the President actually said:

“Homes are built for people, not for corporations, and America will not become a nation of renters. That’s why I have signed an executive order banning large institutional investors from buying single-family homes. It’s just not fair to the public. They’re not — they’re not able to buy a house.”

“The house values have gone up tremendously, and [homeowners] have become wealthy…every time you make it more and more and more affordable for somebody to buy a house cheaply, you’re actually hurting the value of those houses, obviously…I don’t want to do anything that’s going to hurt the value of people that own a house. [People] who for the first time in their lives are walking around…very proud that their house is worth $500K, $600K, $700K. Now, if I wanted to really crush the housing market, I could do that so fast, and people could buy houses, but you would destroy a lot of people that already have houses.”

PCE went down, then back up. We got two months of PCE data on Thursday. In October, “core” PCE (which excludes food & fuel prices) dropped from +2.8% YoY to +2.7% YoY. Yay! But in November, it went back to +2.8% YoY. Boo! The good news is that month-over-month growth in the PCE index has been running at just 0.2% over the last 3 months. Annualize that, and you get 2.4% YoY — not far from the Fed’s 2% target.

TP: It’s going to be tough for us to make much progress on inflation over the next couple of months. But the market seems to know that already, with very little hope of a Fed rate cut at the next two FOMC meetings.

Bond and Mortgage Market

With inflation (PCE) remaining above the Fed’s 2% target, the unemployment rate still looking (superficially) low, and GDP running at >4% annually, there is almost zero chance that the Fed votes to cut rates at either the January 28 or March 18 FOMC meetings.

What could change that? One thing could be the BLS’ reworking of the jobs growth statistics using a new and improved birth/death model. This should result in much lower preliminary job numbers (that require fewer revisions), allowing the markets to react to the ‘real’ monthly jobs growth, rather than ‘imaginary’ jobs growth.

Note: After the rate cut on Dec 10, the Fed Funds Rate policy range is now 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

- January 28 FOMC Meeting: 95% probability that the Fed does nothing (unchanged from last week); only a 5% probability of a 25 bps rate cut.

- March 18 FOMC Meeting: 82% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was 78% a week ago). In other words, no cut at either the January or March FOMC meetings. Only an 18% probability that rates are 25 bps below current (was 22% last week), which would imply a 25 bps rate cut at the March 18 meeting.

They Said It

“The only long-term solution to housing affordability is more supply — more single-family homes, more multifamily units, more homes for sale and for rent. A clear indicator of the shortage is that nearly 20% of young adults now live with their parents. Historically, that figure was closer to 10%. That doubling is a direct reflection of the housing deficit we’re facing.” — Robert Dietz, NAHB’s Chief Economist

“Even after accounting for typical seasonal patterns, interpreting in-person home search activity in the winter — especially in December — can be tricky due to public holidays, people taking time off, and wintry weather conditions. We’ll be watching the data in the coming months to determine whether the soft contract signings were a one-month aberration or the start of an underlying trend.” — Lawrence Yun, NAR’s Chief Economist, discussing the surprisingly weak December pending home sales report.

Related posts

The Power of Leverage in Homebuying

FAQ: What are the key costs to budget for when buying a home?

.jpg)

Weekend Talking Points - 'Dissent at the Fed'

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.