.jpg)

It’s been a rough two weeks for mortgage rates, with stronger than expected jobs growth, higher CPI (inflation) and rising bond yields globally. The silver lining for buyers is that home inventory levels continue to rise. That means more choices AND more negotiating power.

No Tax on Home Sales Act. This new bill, if passed, would eliminate capital gains taxes on the sale of a primary residence. In addition to saving millions of homeowners tens of thousands of dollars each, it could also increase the supply of homes for sale (by removing a powerful disincentive to sell).

TP: Under the current law, there is a $250K exclusion for single filers and a $500K exclusion for married filers. But those exclusion amounts were fixed in 1997, when home prices were much lower! It was never the government’s intention to tax Joe Q Citizen on primary home sales.

June CPI moved in the wrong direction. In May, CPI (Consumer Price Index = inflation for you and me) surprised to the downside. In June, that reversed, with annual “headline” CPI accelerating to +2.7% YoY (from +2.4% YoY in May), and annual “core” CPI rising to +2.9% YoY (from +2.8% YoY). Remember: the CPI index gives a massive weighting to shelter costs (~44% of “core” CPI), and the Fed pays more attention to “core” PCE.

TP: The media linked the increase in annual inflation to Trump’s tariffs, but it’s not that simple. The main reason annual inflation increased is what analysts call “tough comps”. In June 2025, “core” CPI only grew 0.2% MoM. But in June 2024, it grew +0.1%. By swapping out June 2024 and swapping in June 2025, you end up with 0.1% growth in the annual figure.

BTW, I was also quite encouraged by the low growth in shelter costs in June (+0.18% MoM, +3.8% YoY), and the drop in prices for both new (-0.3% MoM) and used (-0.7% MoM) cars. These are much bigger items (in terms of their weighting in the index) than the tennis shoes and wall coverings that saw big increases in prices due to (ostensibly) tariff effects.

June PPI was better than expected. In June, “headline” PPI (Producer Price Index = inflation for businesses) was flat MoM — much better than expectations of +0.2% MoM. “Core” PPI was also flat MoM. But…the figure for May was also revised higher (to +0.3% MoM), making the June result look lower. Average the two results and you get +0.1% MoM — not much at all.

Builder confidence edged higher (but remained low). The National Association of Homebuilders’ confidence index climbed one point to 33. But let’s put that in perspective: an index level above 50 indicates a bullish environment. The main issue continues to be affordability (mortgage rates near 7% + high home prices). A new concern is the inventory of existing homes for sales, which is up nearly 30% YoY and approaching pre-pandemic levels.

TP: The homebuilding industry benefited massively from the lack of pre-owned homes available for sale during the pandemic. Now, that’s reversing in many markets. By the way, the median sales price for new homes in May 2025 was $427K. The median listing price for existing homes was $423K.

Bond and Mortgage Market

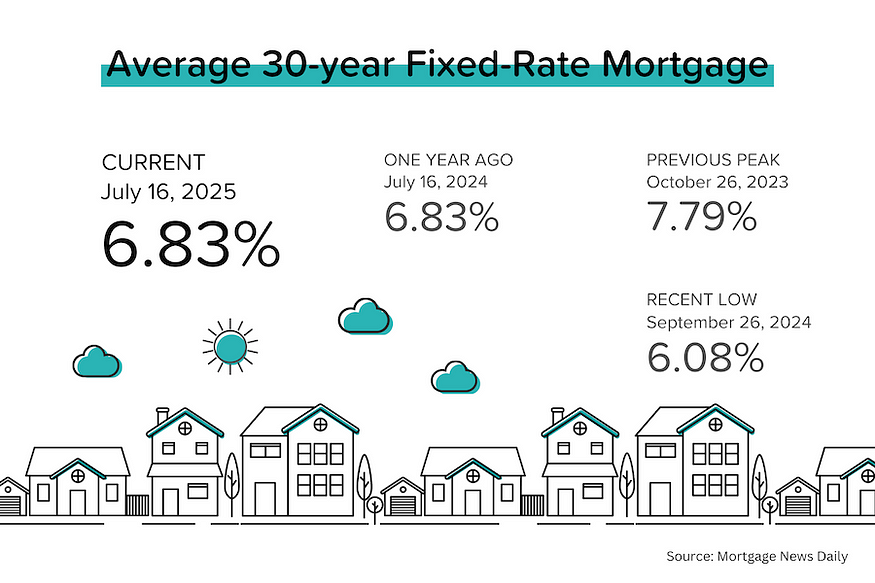

It’s been a rough two weeks for bond yields and mortgage rates. The June BLS jobs report was stronger than expected (falling unemployment rate, +147K jobs added). The June CPI report showed accelerating annual inflation. Oh, and government bond yields have been rising across the globe (UK, Europe, Japan).

While higher bond yields don’t directly translate into higher mortgage rates, they usually trend together. As a result, average 30-yr mortgage rates have moved from 6.67% two weeks ago to 6.85% this week.

Here’s what the Fed Funds Rate futures market is currently pricing in for rate cuts. Note that the current Fed Funds Rate policy range is 4.25–4.50%.

- July 30 FOMC Meeting: 95% probability that the policy rate will remain at 4.25–4.50% (unchanged last week). The June CPI report had little impact.

- September 17 FOMC Meeting: 59% probability that rates will be 25 bps below current (down from 63%). This implies a 25 bps rate cut at this meeting. 38% probability that rates will remain at 4.25–4.50%.

- October 29 FOMC Meeting: 35% probability that rates will be 50 bps below current (down from 39% last week). 16% probability that rates will remain at 4.25–4.50%.

They Said It

“Families who work hard, build equity, and sell their homes should not be punished with massive tax bills. The capital gains tax on home sales is an outdated, unfair burden — especially in today’s housing market, where values have skyrocketed. My bill fixes that.” — Congresswoman Marjorie Taylor Greene

“The passage of the One Big Beautiful Bill Act provided a number of important wins for households, home builders and small businesses. While this new law should provide economic momentum after a disappointing spring, the housing sector has weakened in 2025 due to poor affordability conditions, particularly from elevated interest rates.” — Buddy Hughes, NAHB Chairman

Related posts

.jpg)

Weekend Talking Points - 'Convinced'

.jpg)

Cooling Job Market Fuels Fed Pivot

September 2025 MBS Highway Housing Index

Ready to close more deals?

ListReports automatically delivers personalized marketing collateral to your inbox helping you engage with your customers and prospects.